[ad_1]

A model of this put up was originally published on TKer.co.

Shares rallied final week. The S&P 500 surged 4.7% in what was the most important weekly achieve since June. The index is now up 4.9% from its October 12 closing low of three,577.03. Nonetheless, it’s nonetheless down 21.8% from its January 3 closing excessive of 4,796.56.

When markets are as unstable as they have been, it’s straightforward to get caught up in all of the issues which might be going proper or incorrect in the intervening time.

And whereas there’s nothing incorrect with preserving present on the current, this isn’t the precise mindset for long-term buyers in shares.

“Don’t put money into the current,” Stanley Druckenmiller, the legendary hedge fund supervisor at present working Duquesne Household Workplace, said. “The current just isn’t what strikes inventory costs.”

Druckenmiller famous that that is his No. 1 piece of recommendation for brand spanking new buyers.

In a Sept. 22 episode of the “How Leaders Lead” podcast, Druckenmiller expanded on this (by way of The Transcript):

“I realized this fashion again within the 70s from my mentor [Speros] Drelles. I used to be a chemical analyst. When do you have to purchase chemical corporations? Conventional Wall Avenue is when earnings are nice. Properly, you do not wish to purchase them when earnings are nice, as a result of what are they doing when their earnings are nice? They exit and increase capability. Three or 4 years later, there’s overcapacity they usually’re shedding cash. What about after they’re shedding cash? Properly, then they’ve stopped constructing capability. So three or 4 years later, capability could have shrunk and their revenue margins can be approach up. So, you all the time must form of think about the world the way in which it should be in 18 to 24 months versus now. In the event you purchase it now, you are shopping for into each single fad each single second. Whereas when you envision the long run, you are making an attempt to think about how that is perhaps mirrored in a different way in safety costs.”

That is theoretically sound as principle says the worth of a inventory ought to replicate the current worth of an organization’s future money flows.

Druckenmiller is speaking about choosing shares. However I feel his nonetheless serves as an excellent framework for broadly diversified buyers processing macro data coming from financial knowledge and earnings bulletins.

The labor market is robust 💪

One massive theme of late has been the energy of the labor market. Particularly, the elevated level of job openings indicators the necessity to rent, and the depressed level of layoff activity indicators the need to hang on to employees.

Contemplate these quotes from current earnings calls (by way of The Transcript and RBC Capital Markets):

-

“I might be aware at this level, primarily based on our Q3 efficiency, we’ve seen web hiring amongst our clients. So, we’ve not but seen an emergence of recessionary influence in our business e book of enterprise.” – UnitedHealth Group

-

“We’re seeing optimistic staffing tendencies with 11 straight weeks of web pharmacist head rely will increase.” – Walgreens Boots Alliance

-

“We do not make main cutbacks throughout the plant…We do not see any purpose for excellent draconian measures.“ – Morgan Stanley

Bloomberg reported that Goldman Sachs, Morgan Stanley, Citigroup, JPMorgan Chase, and Financial institution of America all elevated their headcounts in Q3.

Equally, the previous week’s high-level financial reviews broadly confirmed these anecdotes. Preliminary claims for unemployment insurance coverage advantages fell last week and proceed to pattern at low ranges. The Federal Reserve’s October Beige Book stated that employment “continued to rise at a modest to average tempo in most Districts.“ Manufacturing enterprise surveys from the NY Fed and Philly Fed every indicated employment was up of their respective areas in October.

What all this staffing means for the long run 🤔

The resilient labor market means that demand within the financial system continues to be strong.

However that’s the current.

What in regards to the future? What does this imply 18 to 24 months down the street?¹

I feel there are at the least two primary situations to think about.

-

Bearish state of affairs: The financial lull we’re in finally evolves into recession and we’ve an prolonged interval of weak demand. Firms which might be at present rising hiring or refusing to layoff staff might see a pointy drop in earnings as weak income runs into excessive labor prices, and profit margins get crushed.

-

Bullish state of affairs: The financial lull we’re in proves short-lived, and progress quickly accelerates once more. Firms that held on to staff or grew head counts at this time may not need to compete aggressively for workers in what ought to be an more and more aggressive labor market. As a result of they have already got further capability, these corporations will profit from working leverage as income progress comes with increasing revenue margins, which amplifies earnings progress.

What really occurs is dependent upon the place the financial system heads, which itself just isn’t a simple factor to foretell.

However I can’t assist however assume that given the present state of issues, the outlook favors the extra bullish state of affairs. Why? As a result of the message from the financial knowledge and company America is that demand continues to outpace the capability to provide. Contemplate this quote from the Fed’s October Beige Book: “General labor market circumstances remained tight, although half of Districts famous some easing of hiring and/or retention difficulties. Competitors for staff has led to some labor poaching by opponents or competing industries capable of provide greater pay.“

And take into account this from Domino’s: “Staffing stays a constraint, however my confidence in our capacity to resolve lots of our supply labor challenges ourselves has grown over the previous few quarters.”

So demand must fall significantly earlier than corporations discover themselves with an excessive amount of expensive idle labor.

Let’s examine again in 18 to 24 months.

The underside line: Shares are a discounting mechanism, pricing in what’s anticipated to occur and never what’s at present occurring. Whether or not it’s 18-24 months out or 20 years out, being within the inventory market is about betting on a greater future that has but to be realized and priced in. Now, it’s not notably clear what’s to return in 18-24 months. (The lesson of the past 18-24 months is that things can certainly go wrong.) However long-term history could be very constant in educating us that the long-term future always turns out to be better than what we’re experiencing at this time.

–

Extra from TKer:

Reviewing the macro crosscurrents 🔀

There have been a couple of notable knowledge factors from final week to think about:

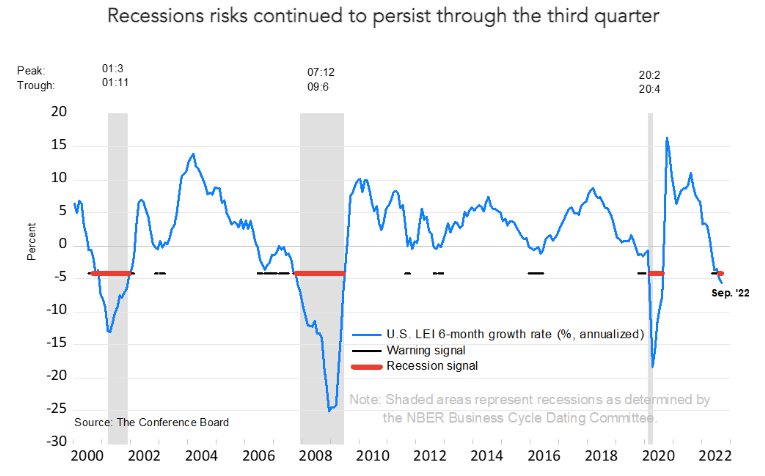

🚨 Recession warning signal. The Conference Board’s Leading Economic Index2 fell in September. The six-month common change was -0.5%, a studying that is traditionally related to recessions. From The Convention Board’s Ataman Ozyildirim: “The US LEI fell once more in September and its persistent downward trajectory in current months suggests a recession is more and more probably earlier than yearend. The six-month progress fee of the LEI fell deeper into adverse territory in September, and weaknesses among the many main indicators had been widespread. Amid excessive inflation, slowing labor markets, rising rates of interest, and tighter credit score circumstances, The Convention Board forecasts actual GDP progress can be 1.5% year-over-year in 2022, earlier than slowing additional within the first half of subsequent 12 months.”

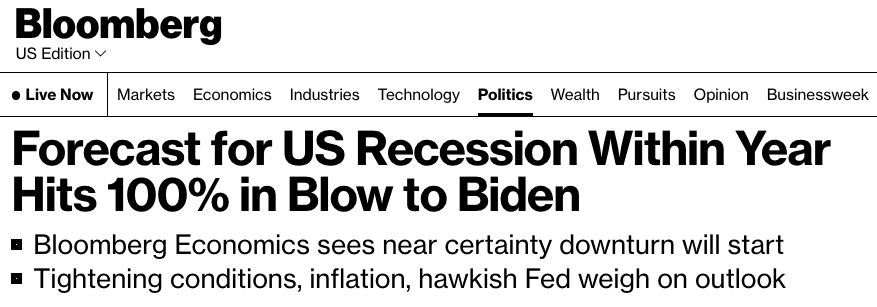

In the meantime, Bloomberg economists estimate there’s a “100%” chance that the U.S. financial system could have entered a recession by October 2023.

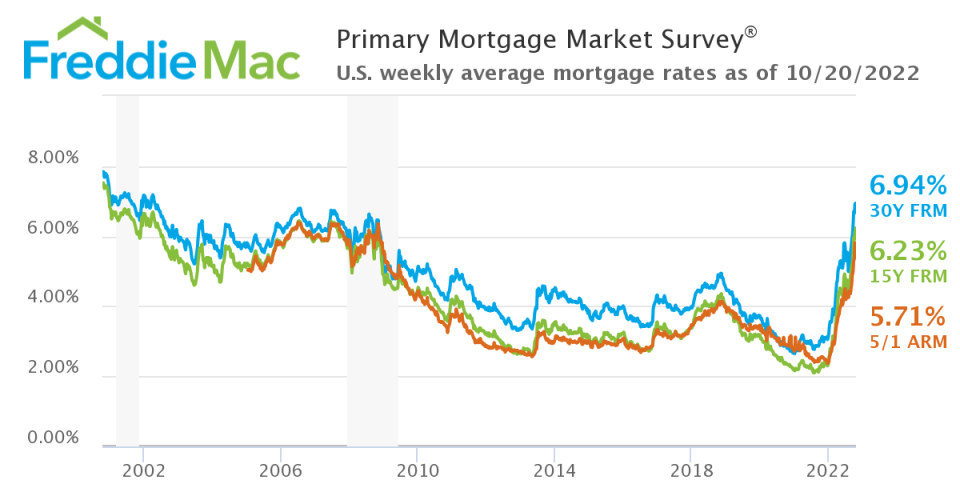

📈 Mortgage charges hold climbing. In line with Freddie Mac, the typical 30-year fixed-rate mortgage rose to six.94%, the very best stage since April 2002.

📉 $2,500 month-to-month mortgage fee will get you much less. Surging mortgage charges and still-high house costs have made shopping for a house unaffordable for a lot of. In line with Bloomberg’s Michael McDonough, a $2,500 month-to-month mortgage fee might get you a $756k house in February 2021. As we speak, it will get you a $455k house.

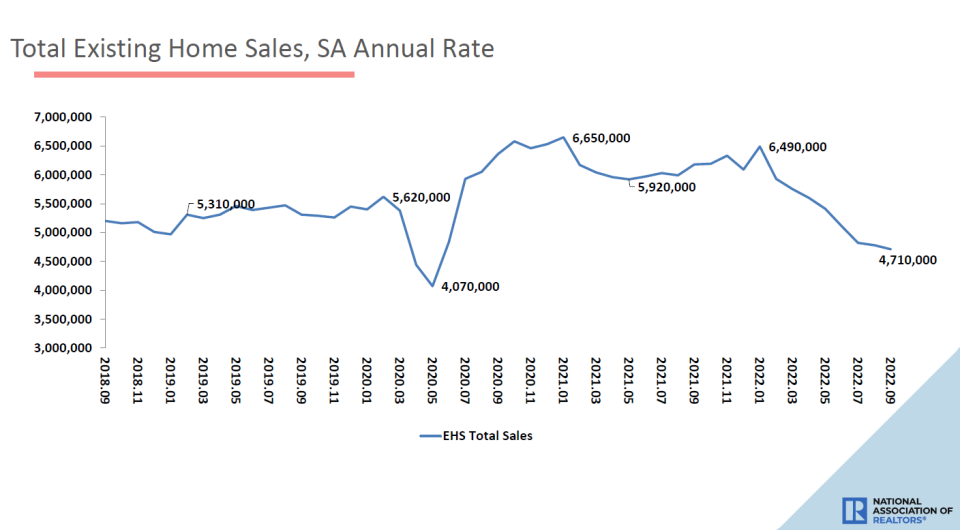

🏘 House gross sales proceed to fall. In line with the National Association of Realtors, gross sales of beforehand owned properties fell 1.5% in September to an annual fee of 4.71 million models. From NAR chief economist Lawrence Yun: “The housing sector continues to endure an adjustment because of the steady rise in rates of interest, which eclipsed 6% for 30-year mounted mortgages in September and are actually approaching 7%. Costly areas of the nation are particularly feeling the pinch and seeing bigger declines in gross sales.“

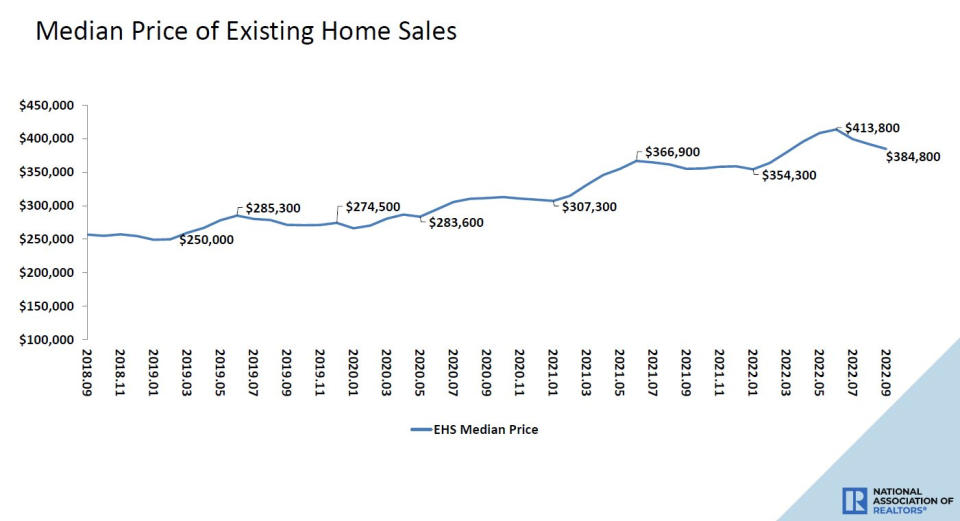

🏘 House costs proceed to fall. The median worth of properties offered fell to $384,800 in September, down from the June excessive of $413,800. Nonetheless, the median worth continues to be 8.4% greater from final 12 months’s stage. To higher perceive why this authorities inflation knowledge seem to lag these tendencies, learn this.

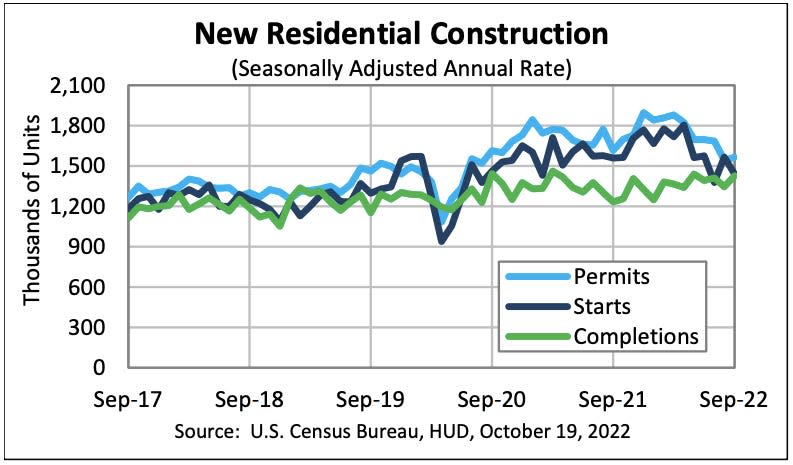

🔨 House building continues to chill. In line with the Census Bureau, the tempo of housing begins September fell 8.1% from August and seven.7% from 12 months in the past ranges. The tempo of latest constructing permits elevated 1.4% from the month prior, however was down 3.2% from a 12 months in the past.

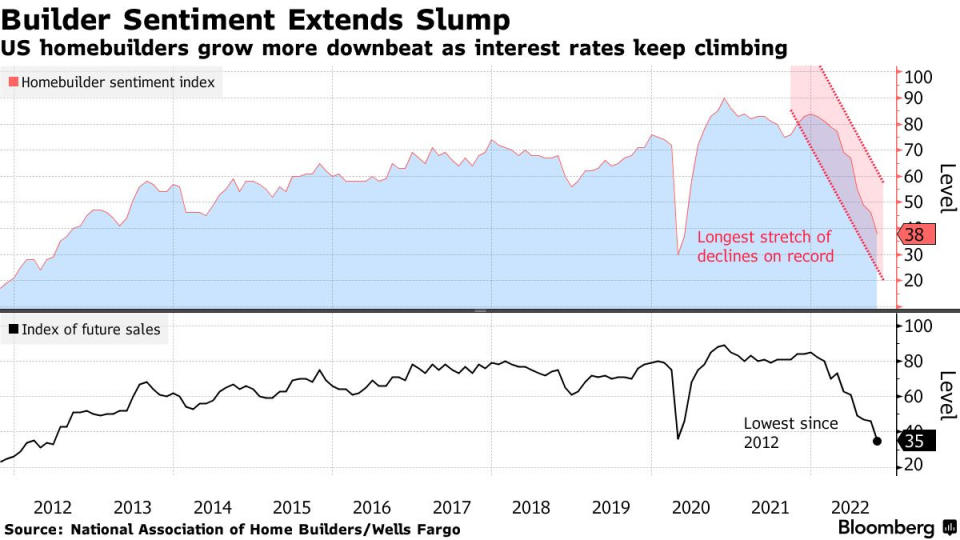

🛠 Builder sentiment goes deeper into the dumps. From the NAHB: “In an additional sign that rising rates of interest, constructing materials bottlenecks and elevated house costs proceed to weaken the housing market, builder sentiment fell for the tenth straight month in October and site visitors of potential consumers fell to its lowest stage since 2012 (excluding the two-month interval within the spring of 2020 at first of the pandemic).“ From NAHB chief economist Robert Dietz: “Whereas some analysts have urged that the housing market is now extra ‘balanced,’ the reality is that the homeownership fee will decline within the quarters forward as greater rates of interest and ongoing elevated building prices proceed to cost out numerous potential consumers.“

🛠 Manufacturing has been holding up. Industrial production activity elevated by 0.4% month over month in September.

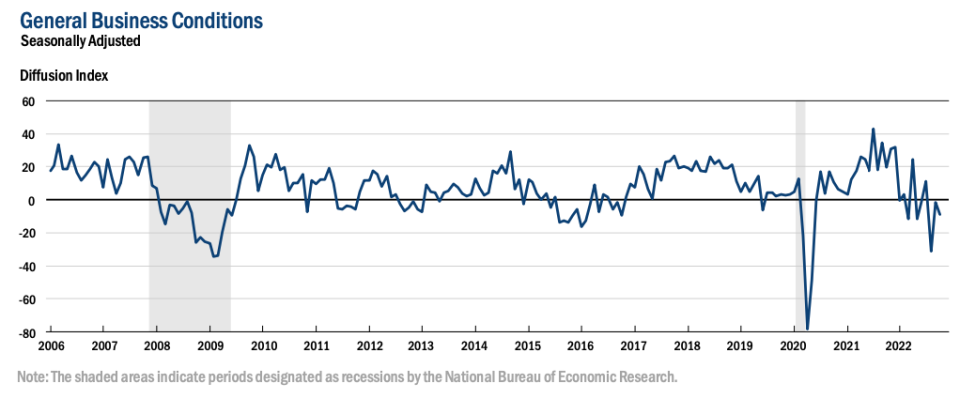

🛠 However manufacturing surveys are extra cautious. In line with the New York Fed’s October Empire State Manufacturing Survey, manufacturing exercise is contracting within the New York space.

And based on the Philly Fed’s October Manufacturing Business Outlook Survey, manufacturing exercise is contracting within the Mideast U.S.

Right here’s JPMorgan on the divergence between the laborious industrial manufacturing knowledge and the delicate manufacturing survey knowledge: “Whereas previous expertise suggests this hole is almost definitely to shut with exercise sinking to reflect the message from the surveys — all of the extra so given the tightening of monetary circumstances — the stunning assist from world items demand provides us pause.“

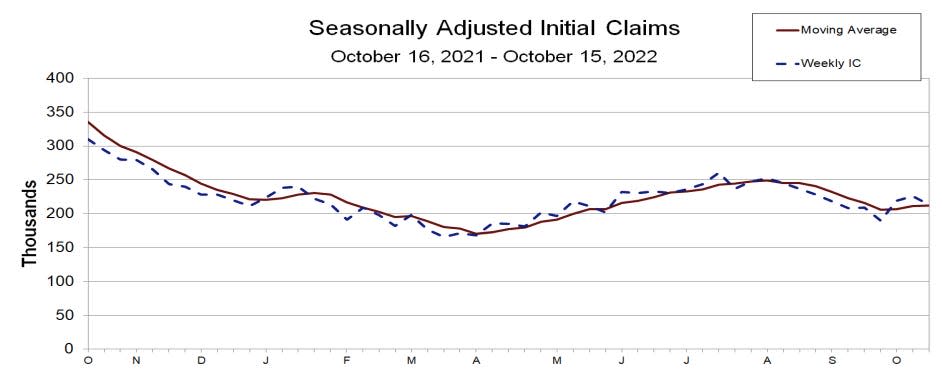

💼 Unemployment claims stay low. Initial claims for unemployment benefits rose to 214,000 through the week ending Oct. 15, down from 226,000 the week prior. Whereas the quantity is up from its six-decade low of 166,000 in March, it stays close to ranges seen in periods of financial growth.

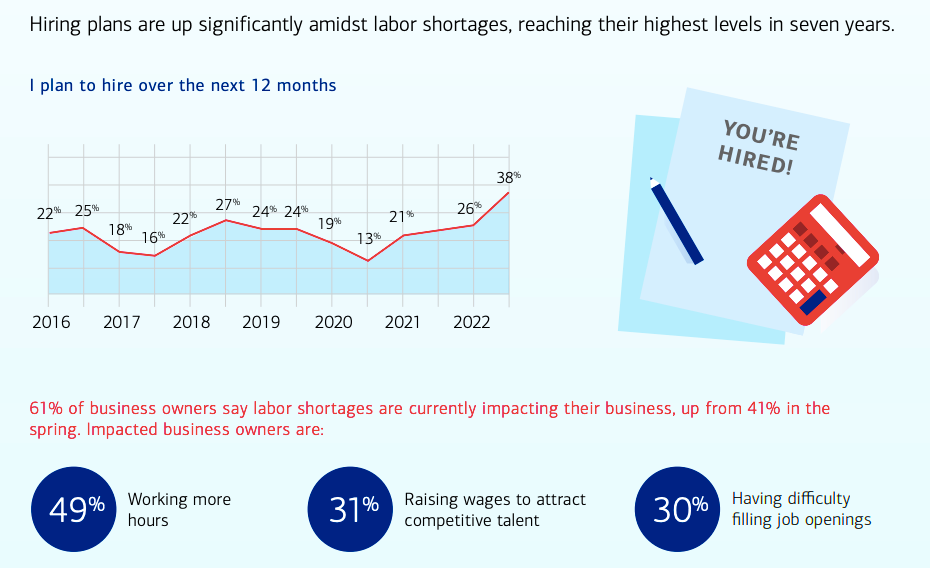

👍 Small companies plan to rent. In line with BofA, a rising proportion of small enterprise house owners plan to rent over the subsequent 12 months.

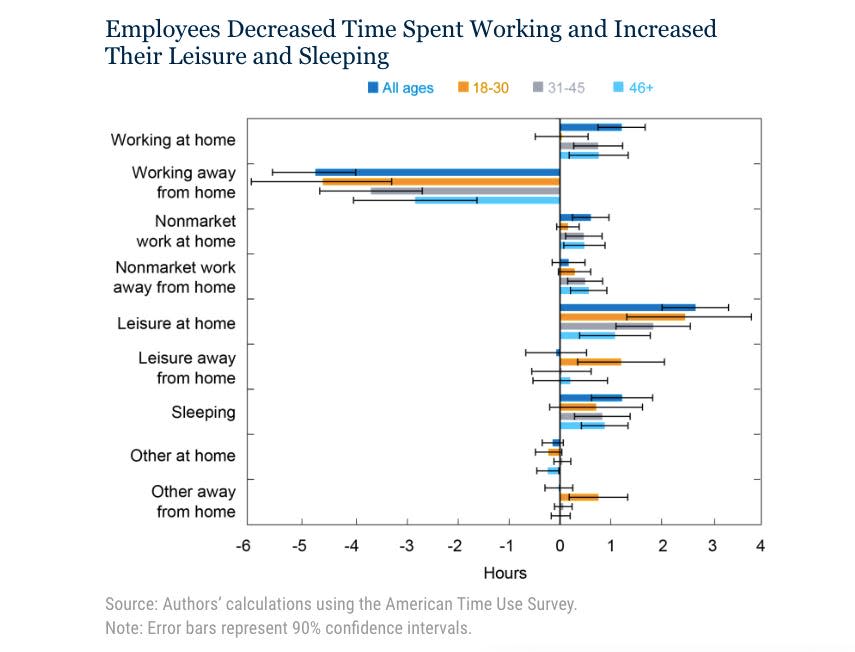

🤾♀️ Much less work, extra leisure. The NY Fed just lately appeared into how People have modified the way in which they use their time because the emergence of COVID-19. From their weblog put up: “First, we discover a substantial fall in time spent working; the lower in hours labored away from house is simply partially offset by a rise in working at house… Second, we see notable will increase in leisure time and sleeping. The rise in leisure was notably pronounced amongst youthful People, who reported spending extra time at social occasions, consuming at eating places or bars, and exercising. Older age teams, then again, tended to allocate extra time to nonmarket work, comparable to actions associated to childcare, the upkeep of the family, repairs, and meal preparation.“

👶 Pandemic “child bump.” From the NBER: “Though fertility charges declined in 2020, these declines seem to replicate reductions in journey to the U.S. Childbearing within the U.S. amongst foreign-born moms declined instantly after lockdowns started — 9 months too quickly to replicate the pandemic’s results on conceptions. We additionally discover that the COVID pandemic resulted in a small “child bump” amongst U.S.-born moms. The 2021 child bump is the primary main reversal in declining U.S. fertility charges since 2007 and was most pronounced for first births and girls below age 25, which suggests the pandemic led some girls to start out their households earlier. Above age 25, the newborn bump was additionally pronounced for girls ages 30-34 and girls with a school schooling, who had been extra more likely to profit from working from house.“

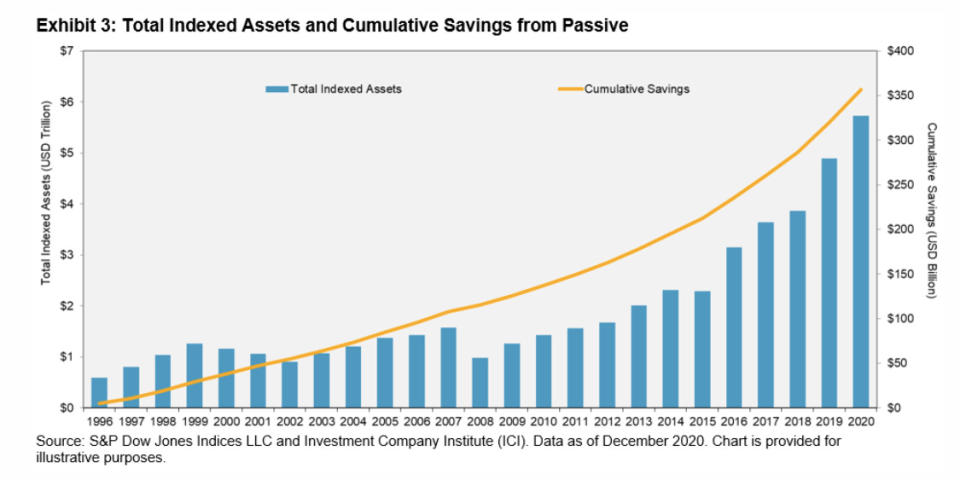

💰 Passive investing financial savings pile up. From S&P Dow Jones Indices: “Among the many many advantages of indexing is its low price relative to energetic administration. As indexing has grown, buyers have benefited considerably by saving on charges and avoiding underperformance. We are able to estimate the payment financial savings every year by taking the distinction in expense ratios between energetic and index fairness mutual funds, and multiplying this distinction by the overall worth of listed property for the S&P 500, S&P 400, and S&P 600. Once we mixture the outcomes, we observe that the cumulative financial savings in administration charges over the previous 25 years is $357 billion.“

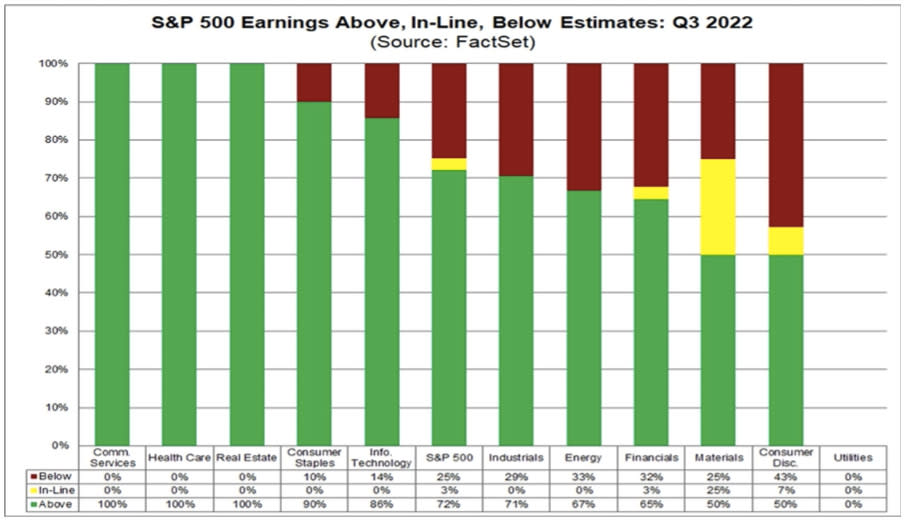

👍 Q3 earnings are beating expectations. From FactSet, “For Q3 2022 (with 20% of S&P 500 corporations reporting precise outcomes), 72% of S&P 500 corporations have reported a optimistic EPS shock and 70% of S&P 500 corporations have reported a optimistic income shock.“

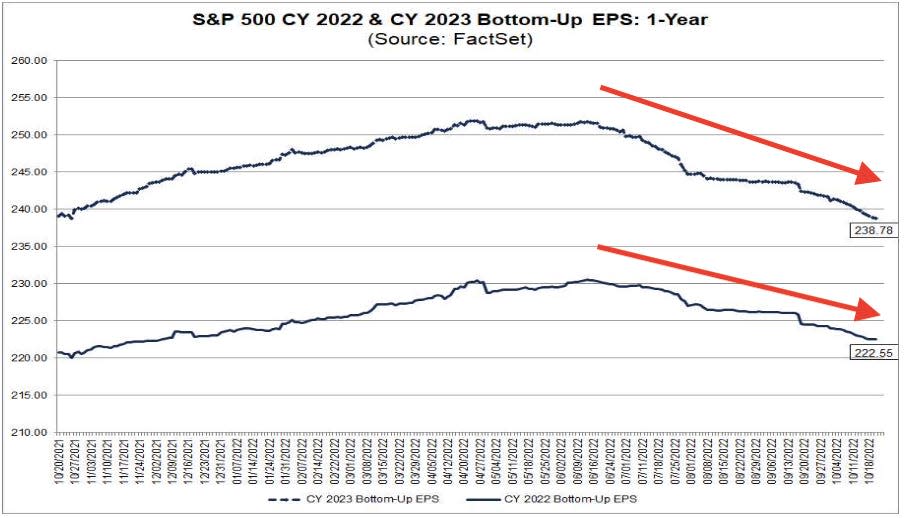

👎 However 2022 and 2023 earnings expectations are coming down. Analysts’ estimates for full 12 months earnings in 2022 and 2023 continue to slip.

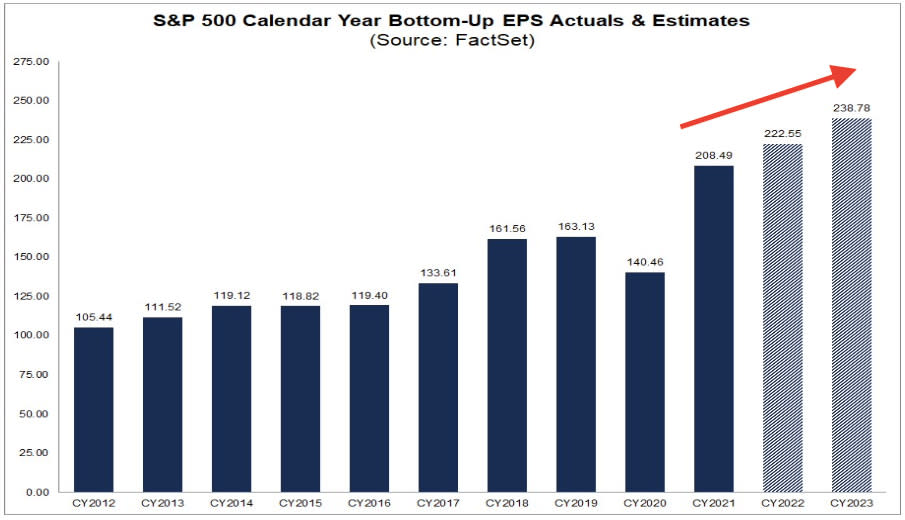

👍 However however: Regardless of the downward revisions to 2022 and 2023 earnings estimates, analysts nonetheless count on earnings to develop 6.7% year-over-year in 2022 and seven.3% in 2023.

Placing all of it collectively 🤔

Tighter financial coverage from the Federal Reserve continues to have an unambiguously adverse influence on the housing market as higher mortgage rates cool activity. But it surely’s additionally having the central financial institution’s supposed impact of cooling prices.

Producers are cautious in regards to the outlook for the financial system, however actual activity remains resilient.

Labor market indicators, in the meantime, proceed to carry up.

Unfortunately, the propensity for sure segments of the financial system to develop is stopping inflation from coming down quicker. And aggregate measures of inflation remain very high.

So prepare for things to cool additional provided that the Fed is clearly resolute in its fight to get inflation under control. Recession dangers will proceed to accentuate and analysts will proceed trimming their forecasts for earnings. For now, all of this makes for a conundrum for the stock market and the financial system till we get “compelling evidence” that inflation is certainly below management.

The excellent news is there’s nonetheless a powerful case to be made that any downturn won’t turn into economic calamity. That is corroborated by the truth that there’s been no collapse in industrial exercise or shopper spending, which has been supported by the resilient labor market and rising incomes.

And whereas markets have had a terrible year so far, the long-run outlook for shares continues to be positive.

For more, check out last week’s TKer macro crosscurrents »

1. In his quote, Druckenmiller speaks about his time as an analyst masking chemical compounds, a comparatively capital intensive trade. Firms on this enterprise put money into very costly amenities and tools with the intention of utilizing all of it for years. These prices don’t go away throughout downturns. Labor prices are a bit totally different in that corporations have the choice to put off staff.

2. Right here’s extra element from the Conference Board: “The LEI is a predictive variable that anticipates (or “leads”) turning factors within the enterprise cycle by round 7 months… The ten parts of The Convention Board Main Financial Index® for the U.S. embrace: Common weekly hours in manufacturing; Common weekly preliminary claims for unemployment insurance coverage; Producers’ new orders for shopper items and supplies; ISM® Index of New Orders; Producers’ new orders for nondefense capital items excluding plane orders; Constructing permits for brand spanking new personal housing models; S&P 500® Index of Inventory Costs; Main Credit score Index™; Rate of interest unfold (10-year Treasury bonds much less federal funds fee); Common shopper expectations for enterprise circumstances.”

A model of this put up was originally published on TKer.co.

–

Extra from TKer:

Read the latest financial and business news from Yahoo Finance

Observe Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube

[ad_2]